In catastrophic injury cases, the cost of long-term care (LTC) is often one of the most significant components of economic damages. Unlike aging-related eldercare, injury-related LTC can last for decades and require intensive medical and support services starting at a younger age. The CDC estimates that injuries sustained in 2019 alone will ultimately cost the U.S. economy $4.2 trillion, with $327 billion attributed to medical care costs. For an injured plaintiff, these expenses can amount to millions of dollars over a lifetime, covering nursing care, home health assistance, rehabilitative therapies, medical equipment, and home modifications.

Because of these enormous costs, forensic economic analysis plays a critical role in litigation. Juries and judges rely on expert testimony and life care plans to determine the true financial burden of an injury, ensuring that damage awards reflect real-world long-term care needs. Without precise financial modeling, plaintiffs risk receiving insufficient compensation, which could shift the financial burden to families or public programs. The Knowles Group specializes in quantifying long-term care costs, providing courts with accurate, data-driven projections that shape legal outcomes.

The Role of Forensic Economists in Quantifying Long-Term Care Expenses

Forensic economists play a key role in translating an injured person’s care needs into quantifiable, courtroom-ready evidence. Their work ensures that long-term care (LTC) expenses are accurately projected, adequately valued, and legally defensible in settlement negotiations and trial proceedings.

How Forensic Economists Assess Long-Term Care Needs

Forensic economists work alongside life care planners and medical experts to determine the frequency, duration, and cost of future care services required due to an injury. The process typically follows these steps:

- Medical Expert Testimony: A treating physician or medical specialist testifies about the injured person’s long-term medical needs, including necessary treatments, therapies, and care requirements.

- Life Care Plan Development: A life care planner creates a detailed roadmap of anticipated needs, such as:

-

- Attendant care (e.g., hours per day of nursing or in-home assistance)

- Therapy sessions (e.g., physical, occupational, and speech therapy)

- Medical equipment replacements (e.g., wheelchairs, ventilators)

- Facility care needs (e.g., skilled nursing, assisted living)

-

- Forensic Economic Analysis: After the life care plan is developed, forensic economists attach costs and perform financial modeling to determine the total financial impact of the injury over a lifetime.

This method ensures that projected costs are grounded in data and economic principles, preventing speculative or exaggerated figures from distorting the damages award.

Accounting for Inflation and Present Value in LTC Costs

A critical task for the forensic economist is adjusting future costs for inflation and present value to reflect:

- Medical Cost Inflation: Health care costs tend to rise over time, so economists account for medical cost inflation to avoid underestimating future expenses.

- Present Value Discounting: Any award will be paid as a lump sum upfront, so expert forensics must discount future costs to their present value to ensure the plaintiff receives the financial equivalent of what care will cost when needed.

How Present Value Calculations Work

In practice, economists will project annual care costs year-by-year (often using life tables to estimate duration of care), then apply a discount rate to each year’s cost to reflect its value in today’s dollars.

The result is a present-value lump sum that, if prudently invested, should cover future care expenditures.

Forensic economists must choose appropriate discount rates (sometimes guided by case law or statutes) and may testify about the methodology. Courts in many jurisdictions require that juries be instructed on present-value discounting for future damages. One example illustrates how Ohio courts have held that reducing future care costs to present value lies within the province of the jury, even if no economist explicitly does the math on the stand.

In all cases, the economist aims to provide a “precise, objective analysis” that supports fair compensation. By quantifying life care plans, projecting growth in medical prices, and applying sound financial techniques, forensic economists ensure that long-term care needs are neither overstated nor undervalued in legal claims.

Key Drivers of Long-Term Care Costs in Injury Cases

Long-term care (LTC) costs vary widely based on various factors. Injury severity, care setting, and geographic location are among the most impactful. Understanding these factors is essential for accurately estimating economic damages in injury cases.

Injury Severity and Type

The type and severity of an injury are fundamental drivers of long-term care costs. Catastrophic injuries that cause permanent disabilities (such as spinal cord injuries, severe traumatic brain injuries, or multiple traumas) typically incur substantially higher ongoing costs than less severe injuries.

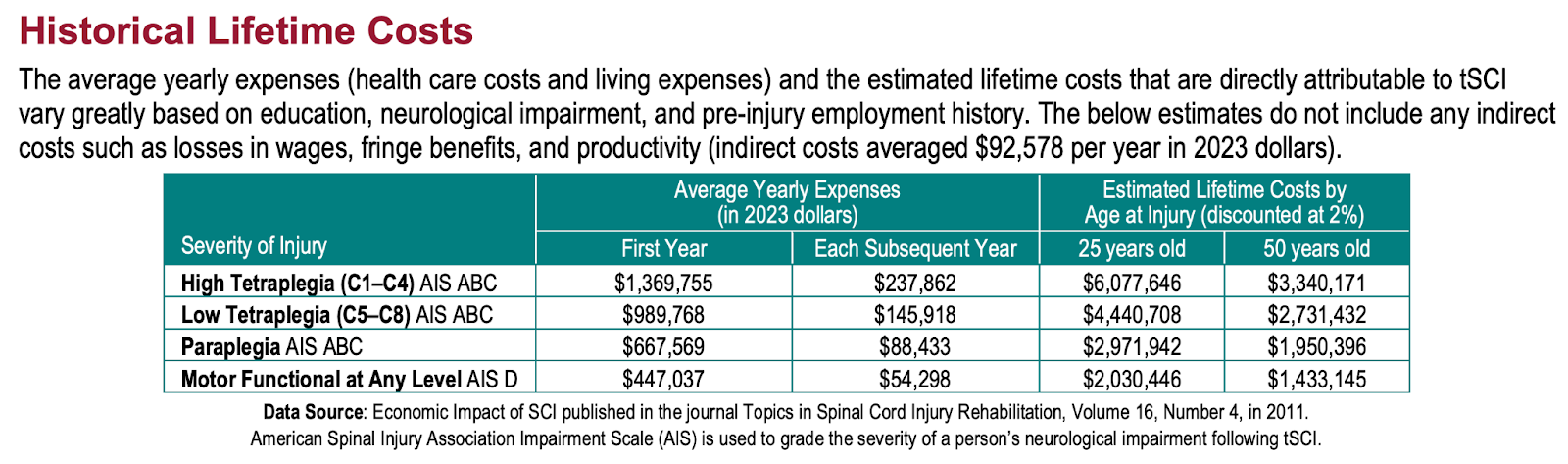

For instance, a person paralyzed from a high cervical spinal cord injury will need a lifetime of intensive personal care, specialized medical equipment (e.g., ventilators or power wheelchairs), home modifications, and frequent medical monitoring. The table above provides data from the National Spinal Cord Injury Statistical Center illustrating that a patient with high tetraplegia (quadriplegia at the C1–C4 level) incurs about $1.37 million in expenses in the first year post-injury and $238,000 in each subsequent year on average. The estimated lifetime costs directly attributable to such an injury are over $6.0 million if injured at age 25 (and about $3.3 million if injured at 50, reflecting fewer remaining years).

Even “moderate” injuries can be extremely costly over a lifetime – for example, a person with moderate traumatic brain injury (TBI) may require cognitive rehabilitation, assisted living, and therapies for years, leading to lifetime care costs that studies have placed in the hundreds of thousands to millions of dollars range. Indeed, experts note that damages for severe traumatic brain injuries can reach eight figures when lifetime care is factored in.

Broadly, injuries that result in a more significant loss of function (paralysis, severe cognitive impairment, etc.) drive higher LTC costs because they necessitate more hours of care and specialized services. In contrast, someone with a less severe injury (e.g., partial mobility loss) might eventually transition to lower levels of care or regain some independence, reducing long-term costs.

Care Setting (Home-Based vs. Institutional Care)

The setting in which long-term care is provided dramatically affects cost. Options range from in-home care (paid caregivers or family members assisting at home) to community-based services (adult day health programs, etc.) to institutional settings like assisted living facilities, skilled nursing facilities, or long-term acute care hospitals. Each comes with a different price tag.

Home-Based Care

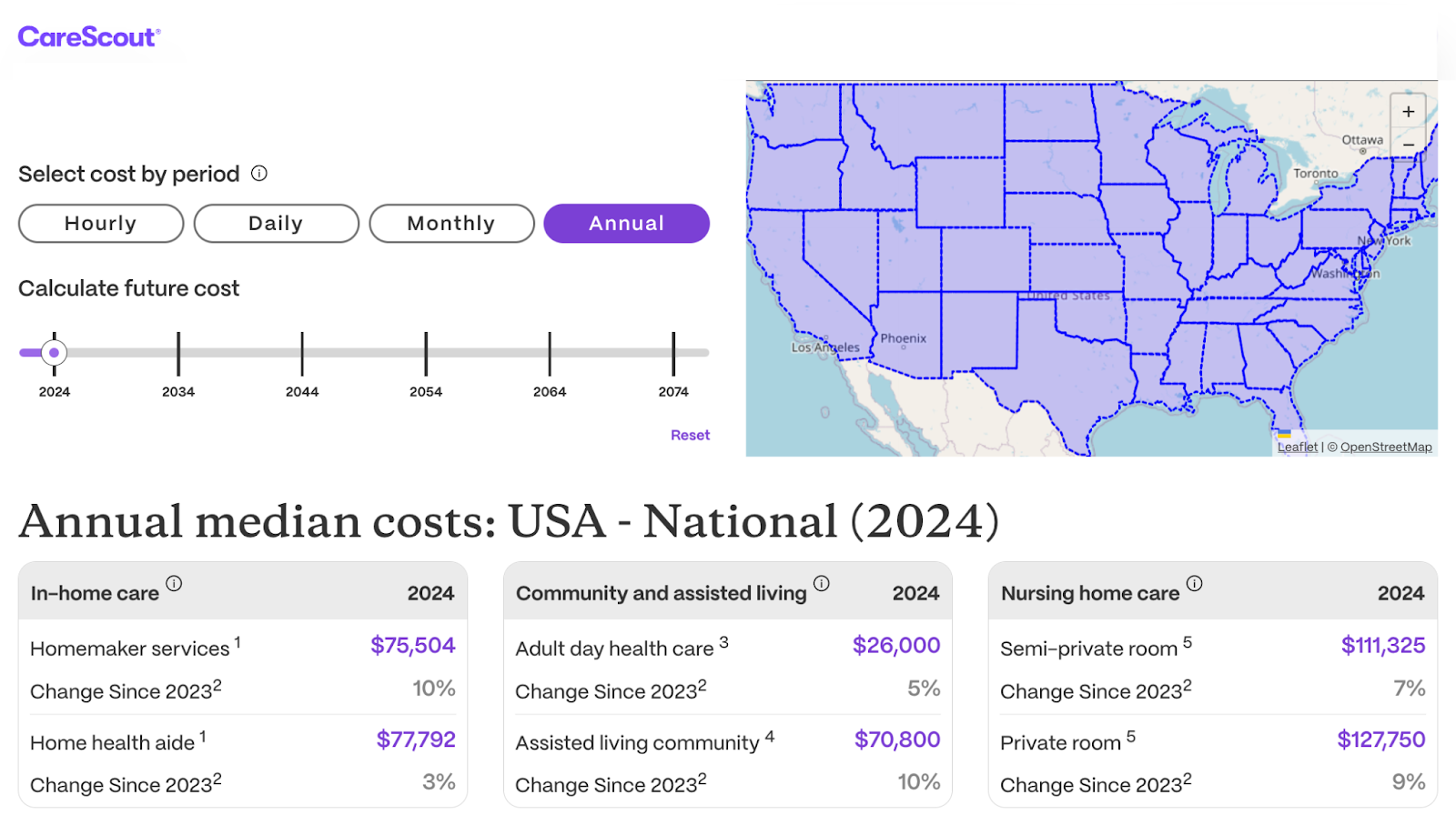

Patients and families often prefer home-based care, which can be cost-effective for moderate needs. However, it still carries substantial expense when skilled services or many hours of help are required. According to industry surveys, the median cost for a home health aide in the U.S. will be about $77,700 annually in 2024, translating to roughly $30–$33 per hour on average. The projected cost will be about $104,500 annually by 2034 (assuming ~44 hours of care per week).

Institutional Care: Assisted Living, Nursing Homes, and Long-Term Hospitals

By contrast, facility care provides around-the-clock supervision at a higher annual cost. A private room in a nursing home now carries a national median cost of about $127,750 per year in 2024. Even a semi-private nursing facility bed costs around $111,300 annually. Assisted living facilities (which offer a lower level of medical care than nursing homes) average slightly less, roughly $71,000 per year nationally, but can vary widely.

It’s important to note that these figures have been climbing each year. For example, from 2020 to 2021 alone, the median cost of a home health aide jumped 12.5%, reflecting rising wages and pandemic-related pressures, and assisted living rates went up ~4.6%.

Over the past five years, annual increases for most LTC services have averaged 2%–6%, often outpacing general inflation.

Geographic Variations

Long-term care (LTC) costs vary significantly from state to state and even within regions of the same state. Factors such as local wages, cost of living, demand for healthcare workers, and state regulations all contribute to these differences.

Attorneys and forensic economists must account for these regional cost variations when calculating damages. Using national averages can misrepresent the financial burden an injured plaintiff faces.

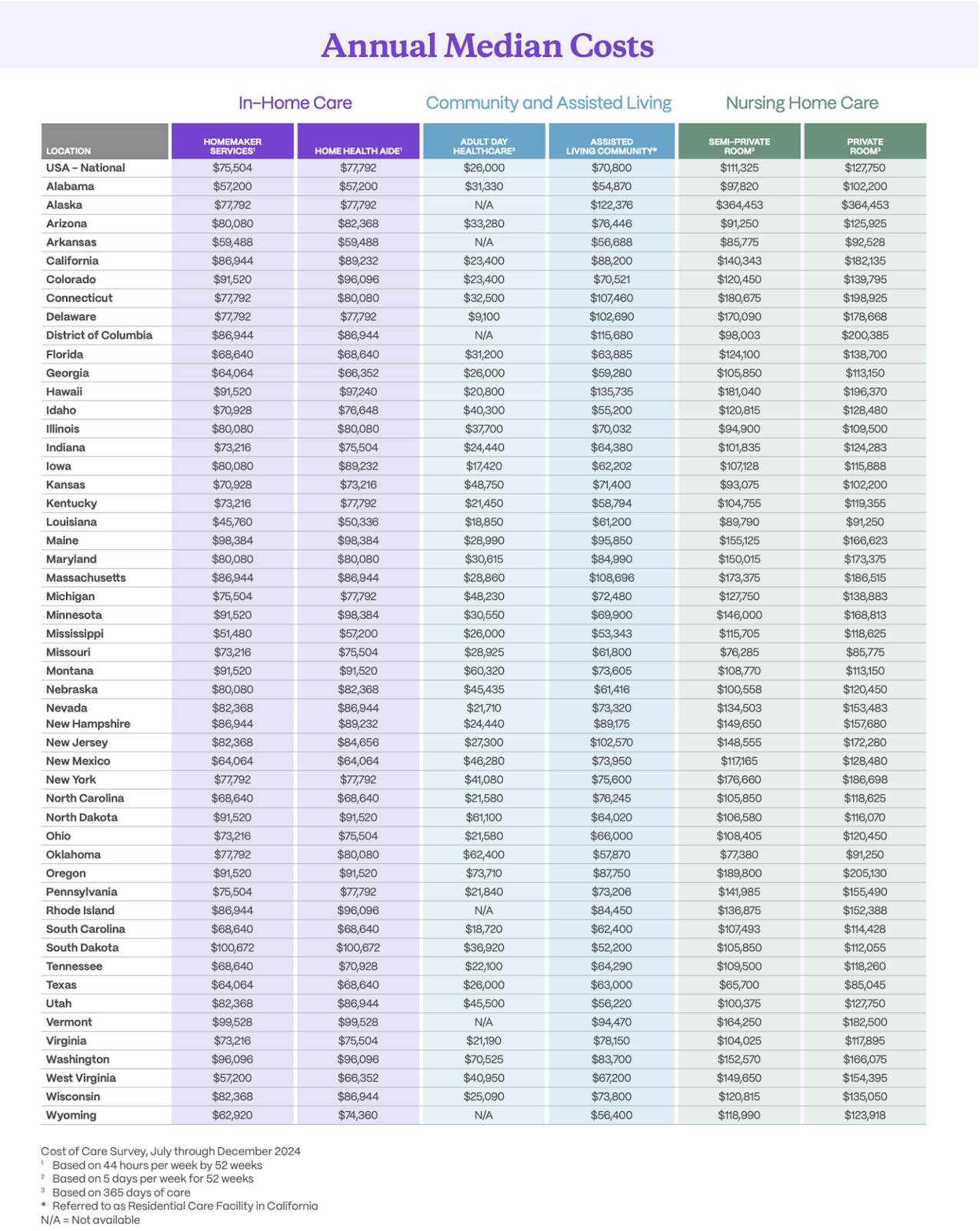

According to Genworth’s national survey, the median annual price of a private nursing home room in 2024 ranged from about $85,775 in Missouri (the lowest state) to over $364,000 in Alaska (the highest). Assisted living facility fees show similar disparities – about $4,445 monthly in Mississippi versus $8,670 monthly in Washington, D.C. Even within the same state, urban areas have higher rates than rural areas. For instance, a home health aide in a major metropolitan area might charge double what a smaller town does.

These geographic cost variations are crucial when projecting long-term care expenses in litigation – the location of care (where the injured person resides or will receive care) must be factored into the valuation. Courts have recognized that using national averages may misstate the true cost if an individual lives in a high-cost region. Moreover, some plaintiffs relocate to access better care or lower costs, further complicating estimates.

Forensic economists often use regional cost databases (such as the Genworth Cost of Care Survey or state labor statistics) to tailor their projections to the appropriate locale. However, they must also consider that geographic cost differences can persist or widen over time. For example, states with caregiver shortages or higher minimum wages may see faster increases in LTC costs.

In sum, where care is delivered is a key driver of cost, alongside what care is needed – a fact that experts and courts carefully consider when evaluating long-term care in injury cases.

Case Studies: Long-Term Care Cost Evaluations in Injury Litigation

In litigation practice, long-term care cost calculations are used to paint a detailed financial picture of an injury’s impact and to justify monetary damages.

Plaintiffs’ attorneys will typically present evidence of a life care plan – often through an expert life care planner or physician – enumerating every foreseeable cost: daily nursing assistance, medications, medical equipment replacements, home renovations for accessibility, therapy sessions, visits to health care providers, etc.

A forensic economist (or sometimes the life care planner in tandem with an economist) will then testify to the present value of these future costs. This comprehensive approach helps the trier of fact (jury or judge) understand the tangible consequences of the injury in dollar terms. Such evidence makes the future damages concrete and can be pivotal in securing adequate awards.

Real-world case outcomes demonstrate the weight given to long-term care evidence. In personal injury cases involving paralysis or brain damage, it’s common for life care plan damages to reach into the millions.

Case Study #1: $120 Million Michigan Birth Injury Verdict

In 2024, a Michigan jury awarded $120 million to the family of a child who developed cerebral palsy due to medical malpractice during birth. The lawsuit alleged that negligence during labor and delivery resulted in oxygen deprivation, causing permanent brain damage. The child’s parents sought damages to cover a lifetime of health care expenses, caregiving needs, and adaptive equipment.

Forensic economic experts presented a detailed life care plan outlining the child’s projected medical needs during the trial. The plan included 24-hour caregiving assistance, specialized medical equipment such as wheelchairs and communication devices, extensive physical and occupational therapy, and home modifications to accommodate mobility limitations. Financial experts’ testimony demonstrated that these costs would accumulate over the child’s projected 51-year life expectancy, significantly increasing the total damages.

The verdict underscored the weight given to economic projections in medical malpractice cases. The state’s Medicaid program even intervened, citing the significant costs it had already incurred and the anticipated financial burden of continued care. This case highlights how forensic economic testimony can justify massive awards by demonstrating the real financial impact of long-term care needs.

Case Study #2: $229.6 Million Baltimore Brain Injury Verdict

In 2019, a Baltimore jury awarded a record-breaking $229.6 million to the family of a newborn who suffered permanent brain damage due to medical negligence. The hospital was found liable for delaying an emergency C-section, which led to severe cognitive impairment and lifelong medical dependency.

Expert witnesses presented a comprehensive life care plan detailing the costs of home-based future medical care, ongoing therapy, assistive devices, medications, and specialized treatments. The plaintiff’s attorneys emphasized the child’s need for round-the-clock medical supervision and assisted living arrangements, arguing that the financial burden would extend for decades.

Forensic economists calculated these medical expenses’ present and future value, which became a focal point in the trial. The jury’s decision explicitly included the lifelong costs of care, reinforcing how economic damage assessments shape high-value malpractice verdicts. This case demonstrated the role of forensic experts in converting an injury’s long-term impact into tangible, data-driven financial projections that help juries understand the true cost of care.

Case Study #3: Hypothetical Spinal Cord Injury Settlement

A 19-year-old college student sustained a spinal cord injury in a car accident, resulting in complete paraplegia. The accident was caused by a commercial trucking company’s negligence, leading to a lawsuit seeking compensation for medical bills, lost earning potential, and long-term care costs.

The plaintiff’s legal team presented a forensic economic analysis estimating the total lifetime cost of care. Initial hospitalization and rehabilitation were projected at $700,000, with ongoing annual care expenses of $90,000 for medical equipment, home modifications, and daily caregiving. Given the plaintiff’s expected lifespan of 50 additional years, the total lifetime medical costs were estimated at $3.5 million.

Rather than proceeding to trial, the case settled for $7 million, with $4 million allocated explicitly to future medical treatment and caregiving needs. The settlement included the creation of a structured medical trust, ensuring that funds would be available throughout the plaintiff’s lifetime. Courts overseeing such settlements often rely on forensic economic testimony to confirm that the amount set aside is sufficient to meet the injured party’s ongoing needs.

Legal Precedents in Assessing Long-Term Care Costs

Courts have developed jurisprudence for assessing and presenting long-term care damages. Legal precedent encourages a thorough but realistic assessment of long-term care costs in injury claims.

Courts expect credible expert evidence to support the need and cost of future care, and they impose guardrails (like present value rules and evidentiary limits on collateral sources) to ensure awards reflect economic reality. As the population of injury survivors with long-term needs grows and healthcare costs evolve, this area of forensic economics and law continues to develop.

Nonetheless, the combination of objective data, expert economic analysis, and clear legal standards helps courts arrive at fair valuations of long-term care costs, providing injured individuals the financial means to access necessary care for as long as needed. A few key principles and precedents include:

“Reasonable Value” of Future Care

Courts generally require that plaintiffs prove the reasonable value of future medical expenses resulting from the injury. This means damages should reflect the cost of care in the relevant market without being inflated or speculative.

Under the collateral source rule, evidence of insurance or government benefits is historically excluded – juries are told to consider the value of care, not who pays. However, recent case law in some jurisdictions has begun to allow evidence of insurance reimbursement rates or benefits when calculating future costs, especially in medical malpractice cases. For instance, in Cuevas v. Contra Costa County (Cal. App. 2017), a California court held that future medical damages may be based on the discounted rates that insurers (including Medicare/Medicaid or private plans) pay, which can indicate the market rate for services. The court even permitted considering the Affordable Care Act’s mandate for insurance coverage as evidence that the plaintiff could obtain care at insured rates. This was a departure from tradition, justified in part by a California statute (MICRA) that softens the collateral source rule in med mal cases.

More recently, Audish v. Macias (Cal. App. 2024) built on Cuevas: It upheld the admissibility of Medicare reimbursement rates in projecting a plaintiff’s future life care costs, reasoning that using these lower rates (instead of full “billed charges”) did not violate the collateral source rule.

These cases signal a trend in which courts seek to prevent exaggerated future cost claims by anchoring them to real-world pay scales. On the other hand, plaintiff attorneys argue that this can unfairly reduce awards since not everyone will actually have access to discounted rates or insurance in the future. The debate is ongoing, but the clear lesson is that courts scrutinize the basis of cost projections and may allow or disallow specific evidence depending on jurisdiction. Experts must be prepared to justify their cost assumptions as reflecting true market value.

Life Care Plans as Evidence

The use of life care plans as evidentiary support for future care damages is well-established. Courts generally accept life care plan testimony from qualified experts (typically rehabilitation specialists or nurses with expertise in planning care needs) to outline the services an injured person will require.

These plans must be grounded in medical necessity to be admissible. Usually, a treating physician or medical expert will testify that the interventions in the plan (surgeries, therapies, attendant care, etc.) are likely to be needed due to the injury. As one legal article notes, expert testimony is required to show that the items in a life care plan are medically necessary and reasonably certain to be needed in the future.

Once that foundation is laid, the costs for those items can be introduced. Courts in many states have approved this two-step approach:

-

- Medical experts establish the needs

- Economic or care planning experts establish the costs

There have been challenges regarding whether life care planners can testify about costs themselves (since they often gather cost data) or whether an economist is needed. Generally, so long as the methodology is sound, a life care planner can present cost estimates, but an economist’s testimony often bolsters the case, especially for present value calculations.

Some case law also addresses duplication or overlap, ensuring, for example, that if a cost (like a particular therapy) is included in the life care plan, it isn’t double-counted elsewhere. Courts will also look at life expectancy assumptions; defense experts occasionally argue that the plaintiff won’t live as standard tables suggest (due to injury-related mortality) to reduce the total years of care. Each of these factors can become a point of contention, but generally, the life care plan provides the blueprint that courts use to assess what future care is reasonably certain to be needed.

Present Value and Discounting

As discussed, legal precedent in virtually all U.S. jurisdictions requires that awards for future damages be stated in present value terms.

A classic reference is the U.S. Supreme Court’s guidance in Jones & Laughlin Steel Corp. v. Pfeifer (1983), which outlined methods for discounting future earnings to present value and emphasized that not doing so would overcompensate the plaintiff.

While Pfeifer was about lost earnings in a federal case, state courts have mirrored its logic for medical damages. Many states have pattern jury instructions telling jurors to reduce any future cost findings to present value (often with an explanation that a dollar today, if invested, will earn interest). Some states even specify a presumed discount rate or allow jurors to consider inflation and interest offsets (the “total offset” method).

Forensic economists’ testimony is often used to walk the jury through the present value calculation. However, interestingly, some courts have held that an economist’s testimony isn’t strictly necessary for present value – the jury can be instructed and do the calculation if given the proper figures. In Ohio, for example, the Supreme Court in Sahrbacker v. Lucerne Products and an appellate court in Daniels v. Northcoast Anesthesia held that “reduction to present value lies within the province of the jury” and a separate expert isn’t required.

The key point is that courts mandate present-value adjustments one way or another. Failure to reduce a future cost award to present value can be grounds for reversal or remittitur (reduction of the award). Thus, any long-term care cost assessment presented in court must include expert-presented discounting or be explicitly addressed via jury instruction.

Forensic Economist’s Role in Challenging Long-Term Care Cost Claims

While plaintiffs present life care plans to justify their claims, defense teams turn to forensic economists to challenge inflated projections, correct faulty assumptions, and present alternative care models that reduce unnecessary costs. This expert analysis plays a critical role in balancing damages awards, ensuring that plaintiffs receive appropriate compensation without overestimation that could lead to excessive or speculative awards.

- Scrutinizing Life Care Plans for Excessive or Unnecessary Costs: A defense-side forensic economist begins by scrubbing the life care plan for overstatements or non-essential expenses. Line-by-line, they evaluate each projected medical need, therapy, or service to see if it is truly necessary and supported by the medical evidence. Defense experts often argue that some life care plans list treatments or equipment beyond standard care guidelines or the plaintiff’s needs. An expert forensic’s analysis will highlight any such inflated or unnecessary line items, providing the defense with evidence that the life care plan’s cost projections are too high or lack medical justification.

- Challenging Life Expectancy Assumptions: Another pivotal task is examining the life expectancy used in the plaintiff’s calculations. The total cost of an LTC plan is susceptible to how many years of care are assumed. Forensic economists will investigate whether the plaintiff’s expert relied on generic life expectancy tables that might not account for the individual’s injuries. Often, plaintiff life care planners use standard actuarial figures (e.g., average lifespan for someone of the same age/gender) without considering that a severe injury or medical condition can shorten the person’s actual life expectancy. The defense economist can challenge these assumptions as speculative if they inflate the projected lifetime of care beyond what medical science supports.

- Assessing Cost Reasonableness with Real-World Data: Forensic economists bring a market reality check to the claimed costs of care. By researching actual prices in the plaintiff’s locale, they assess whether the prices quoted in the life care plan are reasonable compared to real-world medical and caregiving expenses. Each life care plan item is cross-checked against typical local costs, insurance reimbursement rates, and industry benchmarks. If the plan lists a cost that is substantially higher than what providers in the area charge, it’s flagged as inflated due to cost bias or deviation from standard practice

- Evaluating Alternative Care Options to Reduce Costs: A forensic economist also considers alternative care scenarios that meet the plaintiff’s medical needs at a lower cost. Often, plaintiff life care plans choose the most intensive (and expensive) care settings, which drives up the damages. The defense team, informed by medical experts (through independent medical examinations or consulting physicians), may propose different approaches to caring for the injured person.

- Modeling Present Value and Economic Trends: Finally, a core contribution of forensic economists is translating future costs into present-day dollars using sound financial modeling. Even after trimming excessive items, the remaining legitimate future care costs must be evaluated in economic terms. The economist will project each annual expense over the plaintiff’s anticipated care period and then discount those future costs back to present value. This process accounts for the time value of money so that the plaintiff receives a fair lump sum today that can cover future needs, without overcompensating them.

The result is a more accurate, economically grounded damages figure that reflects present value and relevant economic trends rather than a raw, exaggerated sum of future expenses. This rigorous financial modeling reinforces the defense’s position that any compensation for long-term care should be fair and based on sound economics, not wishful projections.

Reach Out Today to Learn How We Can Help with Your Long-Term Care Case

Long-term care (LTC) costs are often the most significant component of damages in catastrophic injury cases, making accurate financial projections essential. Forensic economists play a key role in valuing life care plans, adjusting for inflation, and applying present value discounting to ensure fair compensation. At the same time, defense teams challenge these estimates by questioning life expectancy, treatment necessity, and cost assumptions, making expert economic testimony critical in litigation.

Precise LTC cost evaluations can make or break a case in settlement negotiations or a trial. The Knowles Group provides data-driven forensic economic analysis to support strong, defensible claims. Contact us today to learn how our expertise can help secure accurate long-term care compensation.