In legal cases involving lost earnings, such as those related to personal injury, employment disputes, or wrongful death, economic damages often extend beyond base wages. Certain fringe benefits, like health insurance, retirement contributions, bonuses, and paid time off, can represent a significant share of an individual’s total compensation. In many industries, these benefits account for 20% to 30% of total earnings.

Forensic economists are frequently called upon to calculate economic damages, quantifying the value of lost or foregone benefits as part of a comprehensive damages assessment. In this article, we explain what types of fringe benefits may be included in an economic damages analysis, how they’re typically valued, and why they matter in assessing a reasonable settlement.

Fringe Benefits and Their Role in Economic Damages

Fringe benefits are forms of non-wage compensation that employers provide in addition to regular earnings, often representing a substantial portion of an employee’s total compensation. These damages can hold significant economic value in the context of litigation. When they are regularly provided and can be valued using credible data, expert forensics include fringe benefits in their economic damage assessments. The Bureau of Labor Statistics’ (BLS) Employer Costs for Employee Compensation (ECEC) data set breaks fringe benefits into five primary categories.

Paid Leave

Paid leave includes compensation employees receive while not actively working, such as during vacation, holidays, personal leave, or when they are out due to illness. These benefits are standard in many full-time employment arrangements and may be lost or reduced due to termination, injury, or wrongful employment action.

The value of paid leave is typically measured using the employee’s regular rate of pay and can represent a recurring economic loss over time. Paid leave benefits include:

| Benefit | Description |

|---|---|

| Vacation leave | The employee receives pay while taking pre-approved days off from work for personal use or rest. |

| Sick leave | The employee continues to receive wages during short-term illness or medical appointments. |

| Personal leave | Paid time provided for personal matters not covered by vacation or sick leave, often at the employee’s discretion. |

| Holiday pay | The employer pays the employee for standard holidays (e.g., New Year’s Day, Thanksgiving) when business operations are closed. |

Supplemental Pay

Supplemental pay is additional compensation provided in addition to base wages, typically tied to specific conditions such as working irregular hours, achieving performance goals, or participating in incentive-based compensation structures.

In the context of economic damages, supplemental pay may constitute a recurring or expected component of income and should be included when such earnings are historically documented or contractually promised. Supplemental pay benefits include:

| Benefit | Description |

|---|---|

| Overtime pay | Additional compensation paid when an employee works more than a standard workweek, typically at 1.5 to 2 times the base rate. |

| Shift differentials | Additional income paid for working less desirable shifts, such as nights or weekends. |

| Nonproduction bonuses | Lump-sum payments not directly tied to production output, such as holiday bonuses, signing bonuses, or retention incentives. |

| Performance-based bonuses | Additional compensation tied to meeting performance targets, such as sales quotas, project milestones, or productivity benchmarks. |

| Commission payments | Compensation structured as a percentage of sales or revenue generated; commonly used in sales roles. |

Insurance Benefits

Insurance benefits include employer-provided coverage that protects many employees and their families against financial risks related to health, disability, or death.

These benefits can have substantial economic value, particularly when an employee loses access to them following injury or termination. In damages analysis, forensic economists estimate their value using either the employer’s actual cost or the market cost of equivalent coverage. Insurance benefits include:

| Benefit | Description |

|---|---|

| Health insurance | The employer pays all or part of the premiums for medical, dental, vision, or prescription drug coverage, often including family coverage for dependents. |

| Life insurance | The employer provides or subsidizes a life insurance policy for the employee, typically based on a multiple of the employee’s annual salary. |

| Short-term disability | The employer funds insurance that replaces a portion of income during temporary medical leave or recovery. |

| Long-term disability | The employer funds insurance that provides extended income protection in cases of prolonged or permanent disability. |

Retirement and Savings Benefits

Retirement plans and savings benefits represent employer-sponsored contributions to long-term financial security. These may take the form of defined benefit plans, which promise a specific payout upon retirement, or defined contribution plans, where the employer contributes a set amount to an employee-managed account.

In economic damage calculations, the value of lost retirement benefits may require actuarial projections based on historical contributions, vesting schedules, and expected work life.

| Benefit | Description |

|---|---|

| Defined contribution plans | The employer contributes a fixed amount to a retirement savings plan, such as a 401(k), often with matching provisions. |

| Defined benefit plans | The employer guarantees a fixed monthly benefit at retirement, typically based on years of service and salary history. |

| Profit-sharing plans | The employer makes discretionary contributions to retirement savings accounts based on company profitability. |

| Stock ownership programs | The employer provides equity-based retirement savings through mechanisms such as Employee Stock Ownership Plans (ESOPs). |

The Economic Significance of Fringe Benefits in Lost Earnings Analyses

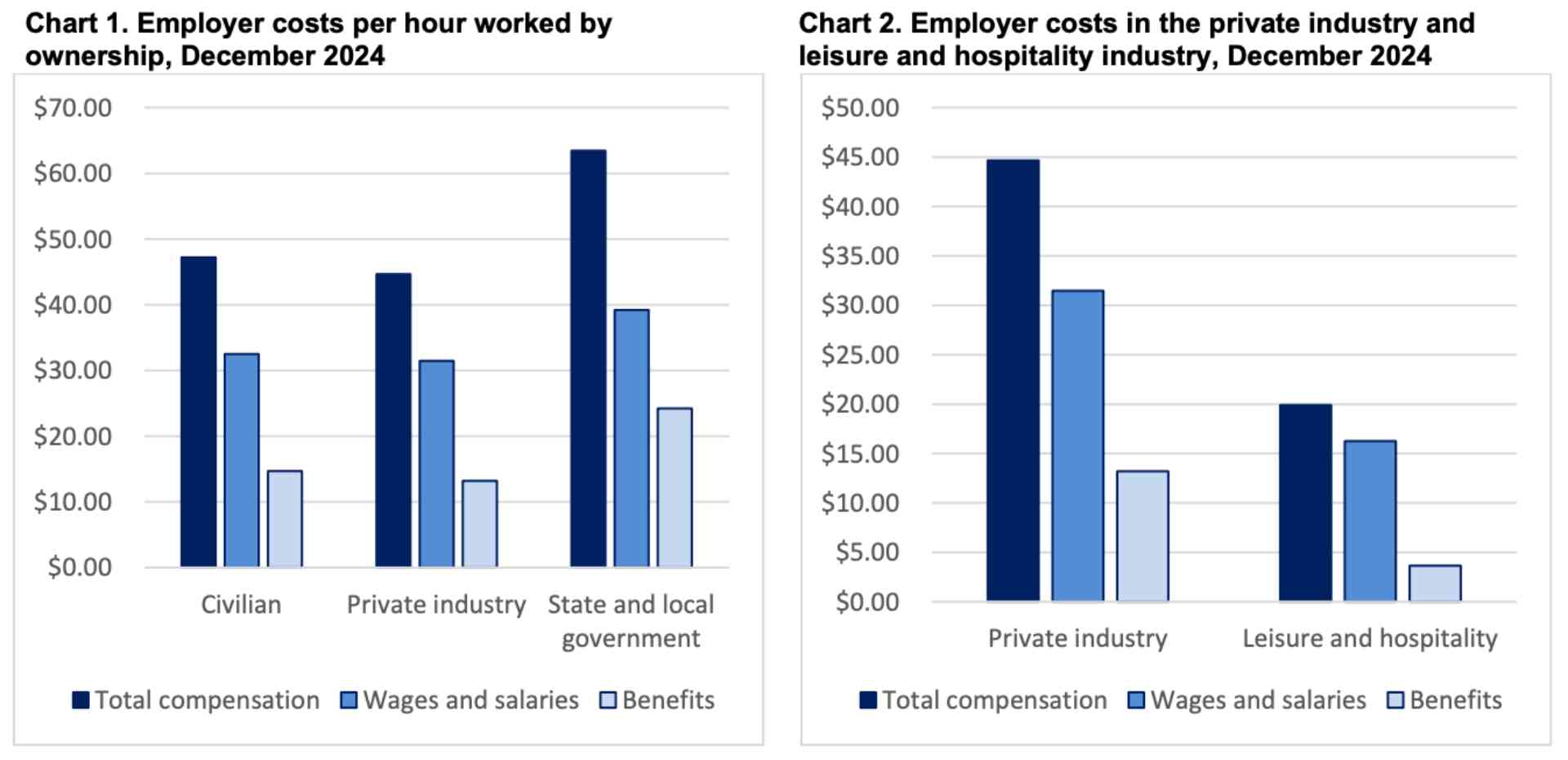

Fringe benefits constitute a significant portion of total compensation and vary considerably across employment sectors. Forensic economists must account for these differences when estimating lost earnings in legal cases. The following table summarizes employer compensation costs by sector based on ECEC data:

| Sector | Total Compensation | Wages & Salaries | Benefit Costs | Benefits as % of Total | Key Observations |

|---|---|---|---|---|---|

| Civilian Workers | $47.20/hour | $32.52/hour | $14.68/hour | 31.1% | National average across both private and public sectors; benefits represent nearly one-third of compensation. |

| Private Industry Workers | $44.67/hour | $31.47/hour | $13.20/hour | 29.5% | Slightly lower benefit share; reflects diverse benefit structures in the private sector. |

| State & Local Government | $63.46/hour | $39.22/hour | $24.23/hour | 38.2% | Higher benefit share due to more generous public-sector retirement and healthcare plans. |

| Leisure & Hospitality (Private) | $19.90/hour | $16.25/hour | $3.65/hour | 18.3% | Lowest benefit share; reflects the prevalence of part-time or seasonal roles with limited benefit offerings. |

These figures illustrate how the value of fringe benefits can significantly influence the outcome of a damages analysis. Applying a standardized benefit rate without considering industry context may lead to inaccurate or incomplete valuations.

How Fringe Benefits Are Valued in Different Legal Claims

The value of fringe benefits can vary significantly depending on the legal context, industry, and the individual’s employment history. Forensic economists tailor their benefit valuation methods to the facts of each case, drawing on employer records, market data, and actuarial assumptions to estimate losses. Whether the claim involves a personal injury, employment dispute, or long-term disability, the inclusion of fringe benefits can substantially affect the total damages calculation. The following examples illustrate how fringe benefit losses are identified and valued in different types of legal cases.

Personal Injury and Accident Cases

In personal injury and accident cases, the loss of fringe benefits often represents a significant portion of the plaintiff’s total economic damages. These cases typically involve workers who can no longer perform their job duties due to a temporary or permanent disability. When the injured party was receiving employer-sponsored benefits, such as health insurance, retirement contributions, or paid leave, those other benefits must be valued and added to the total loss calculation.

Example: Valuing Fringe Benefits and Disability Insurance in a Personal Injury Case Involving a Union Construction WorkerIn a personal injury case, a union construction worker is permanently disabled after falling from an unguarded platform. Before the injury, in addition to a $70,000 base salary, his employer provided a comprehensive benefits package that included family health insurance, a 401(k) match, and four weeks of paid vacation annually. Using life expectancy tables and work-life projections, the economist applies discounting to present value to determine the full long-term economic impact of the injury: |

|

| Factor | Value / Description |

| Type of benefits | Health insurance, 401(k) match, paid leave |

| Base annual salary | $70,000 |

| Health insurance value | $18,000 annually ($1,500 per month x 12 months) |

| 401(k) employer match | $3,500 annually (5% of $70,000) |

| Paid leave value | $5,385 annually (4 weeks of wages) |

| Total annual fringe benefit loss | $26,885 annually ($18,000 + $3,500 + $5,385) |

Wrongful Termination and Discrimination

In employment law cases, such as wrongful termination, retaliation, or discrimination, the loss of fringe benefits is often a critical component of the damages analysis. These cases typically involve plaintiffs who were separated from their employer prematurely and may have missed out on a wide range of compensation elements beyond base pay. Forensic economists evaluate not just lost wages but also the benefits the employee would have received had the continuous employment relationship not been disrupted.

Example: Valuing Fringe Benefits in a Wrongful Termination Case Involving a Sales ManagerIn a wrongful termination case, a sales manager is let go shortly after reporting regulatory violations. Before the termination, she received a compensation package that included a $90,000 base salary, a 6% employer 401(k) match, quarterly bonuses averaging $5,000, and annual vesting stock options valued at $15,000. She also had employer-sponsored health insurance valued at $1,200 per month. A forensic economist estimates her annual fringe benefit losses as follows. For elements like stock options, which are not guaranteed, the economist may apply risk adjustments based on the company’s historical practices: |

|

| Factor | Value / Description |

| Type of benefits | Health insurance, 401(k) match, bonuses, stock options |

| Base annual salary | $90,000 |

| Health insurance value | $14,400 annually ($1,200/month x 12 months) |

| 401(k) employer match | $5,400 annually (6% of $90,000) |

| Bonus compensation | $20,000 annually ($5,000 x 4 quarters) |

| Stock option value | $15,000 annually (subject to risk adjustment based on historical practices) |

| Total annual fringe benefit loss | $54,800 annually ($14,400 + $5,400 + $20,000 + $15,000) |

Sexual Assault and Domestic Abuse

In civil claims related to sexual assault or domestic abuse, plaintiffs may experience psychological trauma that disrupts their ability to maintain employment. When this disruption leads to lost jobs or extended medical leave, the economic impact often includes fringe benefits that are no longer available. These cases may also involve early withdrawal from the workforce or reduced future employability, requiring long-term benefit loss projections.

Example: Valuing Lost Fringe Benefits in a Civil Case Involving Sexual Assault and Career DisruptionIn a civil claim involving sexual assault, a high school teacher takes extended medical leave due to post-traumatic stress disorder (PTSD) and ultimately resigns from her position. Her prior compensation included a $75,000 base salary, district-paid health benefits valued at $1,400 per month, 30 days of accrued sick leave, and participation in a state pension system with an 8% employer contribution rate. The forensic economist calculates the first year of fringe benefit losses as follows. Depending on the plaintiff’s medical prognosis, additional long-term benefit losses may be projected: |

|

| Factor | Value / Description |

| Type of benefits | Health insurance, sick leave, retirement contributions |

| Base annual salary | $75,000 |

| Health insurance value | $16,800 annually ($1,400 per month x 12 months) |

| Sick leave value | $8,654 (30 days x $288.46/day, based on $75,000 ÷ 260 workdays) |

| Retirement contribution | $6,000 annually (8% of $75,000) |

| Stock option value | $15,000 annually (subject to risk adjustment based on historical practices) |

| Total annual fringe benefit loss | $31,454 annually ($16,800 + $8,654 + $6,000) |

Methodologies for Valuing Fringe Benefits

Accurately valuing fringe benefits is a critical component of economic damages analysis. The appropriate valuation method depends on the nature of the benefit, the availability of documentation, and the employment context. Forensic economists select from several well-established approaches, each grounded in accepted economic theory and legal standards. In many cases, a combination of methods may be used to support a comprehensive and defensible analysis.

Direct Replacement Cost Method

The direct replacement cost method estimates the market value of a lost benefit by identifying what it would cost the individual to replace that benefit independently. Economists use this approach most commonly in benefits like health insurance, life insurance, and disability coverage, where comparable individual or group market rates are readily available. The replacement cost serves as a practical proxy for the economic value the employer had been providing.

Example: Valuing Lost Health Insurance Benefits Using the Replacement Cost MethodAn employee injured in a motor vehicle accident loses access to employer-sponsored health insurance for twelve months. The employer had been covering 80% of the premium for a family plan costing $2,000 per month. Using the replacement cost method, the forensic economist values the benefit loss as follows: |

|

| Factor | Value / Description |

| Type of benefit | Employer-sponsored family health insurance benefits |

| Total monthly premium | $2,000 |

| Employer contribution percentage | 80% |

| Employer contribution amount | $1,600 per month |

| Duration of loss | 12 months |

| Total value of lost benefit | $19,200 (i.e., $1,600 x 12 months) |

Historical Earnings and Contribution Analysis

When detailed employment records are available, forensic economists may base benefit valuations on the actual amounts previously received or contributed by the employer. This approach uses documents such as pay stubs, W-2 forms, and benefit summaries to establish a historical pattern of compensation. It is especially useful for quantifying recurring benefits, such as 401(k) contributions, bonuses, commissions, or paid time off.

Example: Valuing Lost 401(k) Contributions in a Wrongful Termination CaseA former employee alleges wrongful termination after consistently receiving employer-sponsored 401(k) contributions during their prior employment. The individual provides three years of W-2 forms showing a 6% employer match on an annual salary of $90,000. The forensic economist uses this historical data to estimate the value of lost retirement contributions over a projected five-year employment period, as follows: |

|

| Factor | Value / Description |

| Type of benefit | Employer 401(k) contribution |

| Base annual salary | $90,000 |

| Employer contribution percentage | 6% of annual salary |

| Employer contribution amount | $5,400 per year |

| Duration of loss | 5 years |

| Total value of lost benefit | $27,000 (i.e., $5,400 x 5 years), excluding investment growth or interest |

Benchmarking with Published Data

In situations where employer-specific data is unavailable or incomplete, economists may turn to publicly available benchmarks, most commonly from the BLS ECEC data, which provides average benefit costs by occupation, industry, and sector as a percentage of total compensation. This approach enables economists to estimate benefit values that are reasonable and supportable when documentation is limited or the employment relationship has never been fully established.

Example: Estimating Fringe Benefits Using BLS Benchmark Data After a Rescinded Job OfferAn individual receives a written offer for a full-time position with a base salary of $70,000, but the offer is rescinded before employment begins. Because the individual never received pay stubs or benefit documentation, the forensic economist cannot use employer-specific data. Instead, the economist relies on BLS benchmarks, which indicate that fringe benefits account for 29.5% of total compensation in the private sector. The value of the lost benefits is estimated as follows: |

|

| Factor | Value / Description |

| Type of benefit | General fringe benefits (estimated using BLS benchmarks) |

| Offered base salary | $70,000 |

| BLS benefit share (private sector) | 29.5% of total compensation |

| Estimated total compensation | $99,290 (base salary ÷ 70.5%) |

| Estimated fringe benefit value | $29,290 (i.e., $99,290 – $70,000) |

Actuarial and Present Value Adjustments

Some fringe benefits, particularly long-term retirement benefits like a pension plan, accrue over time and may not be immediately accessible. In these cases, forensic economists use actuarial methods to estimate the present value of future benefits. This involves applying discount rates, life expectancy tables, and work-life expectancy projections to determine the present value of a future stream of benefits in today’s dollars. These calculations are often necessary when evaluating long-term losses or pension-related claims.

Example: Present Value of Lost Pension Benefits Package Following Permanent DisabilityAn employee eligible for a defined benefit pension becomes permanently disabled and can no longer continue working. According to the terms of the pension plan, the employee needed to work an additional 20 years, until age 65, to qualify for a monthly benefit of $2,000 beginning at retirement. The forensic economist applies standard actuarial assumptions, including work-life expectancy, vesting projections, and a 3% discount rate, to calculate the present value of the lost future pension benefit as follows: |

|

| Factor | Value / Description |

| Type of benefit | Defined benefit pension |

| Monthly benefit at retirement | $2,000 |

| Required remaining service | 20 years |

| Age at benefit commencement | 65 |

| Discount rate applied | 3% |

| Adjustments considered | Projected service time, vesting eligibility, and mortality risk |

| Present value of lost benefit | $112,000 |

Treatment of Non-Vested or Discretionary Employee Benefits

Not all fringe benefits are guaranteed. Some, such as performance bonuses, unvested stock options, or profit-sharing contributions, are contingent on future events or employer discretion. In these cases, economists assess the probability of benefit receipt using historical patterns, contract terms, or industry standards. Risk-adjusted modeling or sensitivity analysis may be used to account for uncertainty while still reflecting the potential monetary value of these benefits.

Example: Risk-Adjusted Valuation of Unvested Stock Options After TerminationA technology employee is terminated shortly before their next equity grant vests. The employee had received similar stock option awards in each of the past three years and was scheduled to vest 1,000 additional shares the following year. The forensic economist evaluates the company’s historical grant patterns and current stock performance, estimating a 75% probability that the options would have vested by the end of the year. Using a projected share price of $30, the economist assigns a risk-adjusted value to the lost benefit as follows: |

|

| Factor | Value / Description |

| Type of benefit | Unvested stock options |

| Scheduled vesting amount | 1,000 shares |

| Estimated share price | $30 per share |

| Probability of vesting | 75% (based on historical grant and retention patterns) |

| Risk-adjusted share value | $22.50 per share (i.e., $30 x 75%) |

| Total value of lost benefit | $22,500 (i.e., 1,000 shares x $22.50) |

Challenges and Considerations in Valuing Benefits

Several factors can complicate the accurate valuation of fringe benefits in a legal damages analysis. Forensic economists must evaluate each benefit in context, considering both available data and the likelihood of continued receipt. Key challenges include:

- Employer variability: Employers differ significantly in the scope and consistency of benefits provided. While some offer only core insurance and retirement packages, others include lifestyle benefits (such as childcare, vehicles, and gym memberships) that may impact total compensation.

- Unvested vs. vested benefits: Some benefits, such as stock options or pension credits, may not be fully earned at the time of loss. Economists must assess vesting schedules and apply probability adjustments if benefits were not guaranteed.

- Future benefit cost escalation: Costs for benefits like health insurance often increase over time. Flat-rate projections may undervalue long-term losses unless escalation is accounted for using inflation or trend data.

- Tax treatment: Certain benefits are non-taxable, while others are treated as taxable income. Correctly identifying the tax implications affects net loss calculations and overall compensation modeling.

- Replacement vs. actual cost: The cost to replace a benefit (e.g., private health insurance) may differ from the employer’s historical expense. Economists must decide which approach better reflects economic value in each case.

- Documentation gaps: In cases involving informal employment, job offers, or undocumented benefits, economists may need to rely on benchmark data and clearly state assumptions and limitations.

- Discounting to present value: Long-term benefit losses must be converted into present-value dollars using appropriate discount rates. Inaccurate rates can significantly impact the total damages.

- Overlap with other damages: Some employee benefits may also be covered by different forms of compensation (e.g., government benefits or mitigation income). Careful analysis is necessary to prevent double-counting.

- Qualitative value of benefits: Some fringe benefits, such as generous paid time off or flexible scheduling, provide measurable financial value and also contribute significantly to work-life balance, especially when lost due to injury or job separation.

These challenges underscore the importance of case-specific analysis and transparent methodology in every benefit valuation.

Forensic Economists Account for Fringe Benefits in Comprehensive Damage Calculations

Fringe benefits often represent a significant share of total compensation, and they deserve equal attention in any economic damages analysis. At The Knowles Group, our forensic economists specialize in identifying and valuing these benefits with clarity, accuracy, and supportable data. From employer-paid health insurance to retirement contributions and stock options, we ensure that nothing is overlooked in calculating the full extent of financial loss.

If you’re handling a case involving lost compensation due to injury, wrongful termination, or employment-related disputes, we’re here to help. Contact The Knowles Group today to schedule a free case consultation and learn how our team can support your damages assessment with confidence and credibility.