Interest rates profoundly impact the calculation of economic damages in litigation. As interest rates rise, the stakes become higher for plaintiffs, defendants, and their attorneys, influencing everything from settlement negotiations to courtroom arguments. Understanding how these rates affect damage calculations is crucial, as minor fluctuations can dramatically alter the present value of future economic damages.

Rising interest rates influence the discount rate, the critical component used to convert future financial losses into their present value. The chosen discount rate can significantly shift the outcome of a case, favoring one party at the expense of another.

In this article, we’ll explore how rising interest rates affect economic damage calculations and unpack their impact on personal injury, business, and property-related claims. We’ll also highlight the strategic considerations and legal implications of discount rates, enabling attorneys and their clients to make well-informed, economically sound decisions.

How Interest Rates Affect Economic Damage Calculations

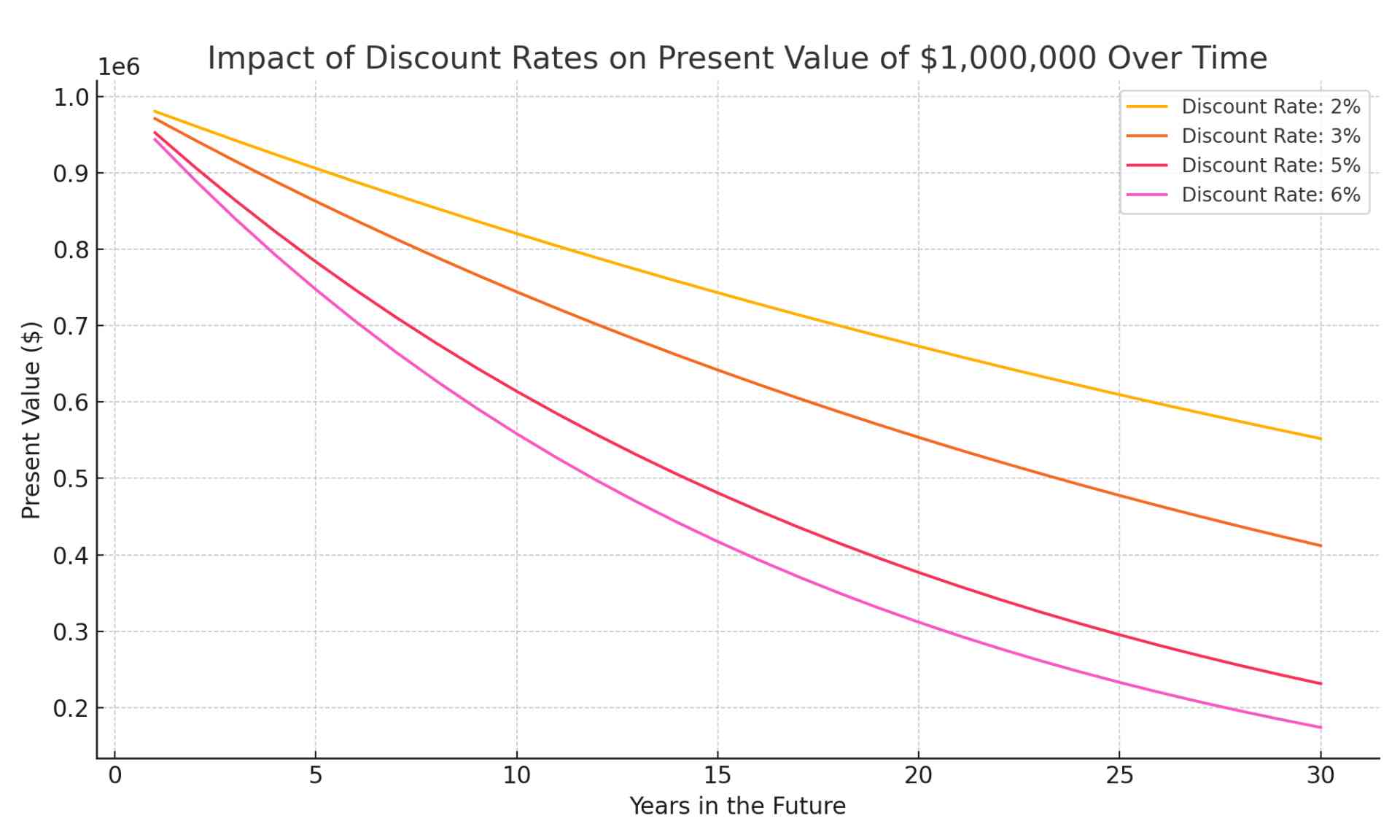

Economic damage calculations quantify the value of losses that will occur in the future. Forensic economists must translate future losses into their present value because these damages are typically awarded in lump sums today. The critical factor in this conversion is the discount rate.

The discount rate is a way to account for the fact that money today is worth more than the same amount in the future, because you could invest it and earn interest. When economists use discounting, they determine the value of a future loss, such as medical bills or lost wages, in today’s dollars. A higher discount rate means future losses are valued less, because the money could have been earning more in the meantime.

Discounting Future Damages to Present Value

Discounting involves determining how much a future sum is worth in today’s dollars. Because a dollar today can be invested and earn interest, it’s more valuable than the same dollar received years from now. The discount rate reflects the time value of money. It represents the rate of return that could reasonably be earned on an alternative investment with similar risk.

In economic damages analysis, this rate converts future losses into their present value, allowing courts to award lump-sum compensation that fairly reflects the value of future harm.

| Future Medical Cost (in 10 Years) | Discount Rate | Present Value | Difference from 2% Rate |

|---|---|---|---|

| $1,000,000 | 2% | $820,348 | — |

| $1,000,000 | 5% | $613,913 | -$206,435 |

For example, a $1,000,000 medical expense 10 years out is worth over $200,000 less when discounted at 5% instead of 2%.

Why the Discount Rate Matters

The discount rate is a powerful lever. Even a slight increase can significantly reduce the present value of long-term economic damages.

| Future Lost Earnings (15 Years @ $100,000/year) | Discount Rate | Present Value | Difference from 3% Rate |

|---|---|---|---|

| $1,500,000 | 3% | $1,193,778 | $0 |

| $1,500,000 | 6% | $971,225 | -$222,553 |

For example, a 3% versus 6% discount rate results in a $222,553 difference in present value for 15 years of lost earnings.

Sensitivity to Interest Rate Changes

The sensitivity of damage calculations to interest rates greatly depends on how far the projected losses extend into the future. Short-term losses are less sensitive, whereas long-term projections become significantly more affected by rising interest rates.

| Plaintiff | Time Horizon | Future Medical Costs | Present Value (3%) | Present Value (6%) | Difference |

|---|---|---|---|---|---|

| A | 5 years | $500,000 | $431,034 | $373,631 | -$57,403 |

| B | 30 Years | $500,000 | $206,231 | $87,055 | -$119,176 |

For example, an increase from 3% to 6% over five years reduces the present value of $500,000 by about $57,000, but over 30 years, that same rate change reduces the present value by more than $119,000.

Impact of Rising Interest Rates on Personal Injury Damages

In personal injury cases, interest rates are applied through discounting to calculate the present value of future damages, making rate fluctuations a critical factor in determining recoverable losses.

To show how rising interest rates affect personal injury and wrongful death claims, we’ll use a hypothetical case:

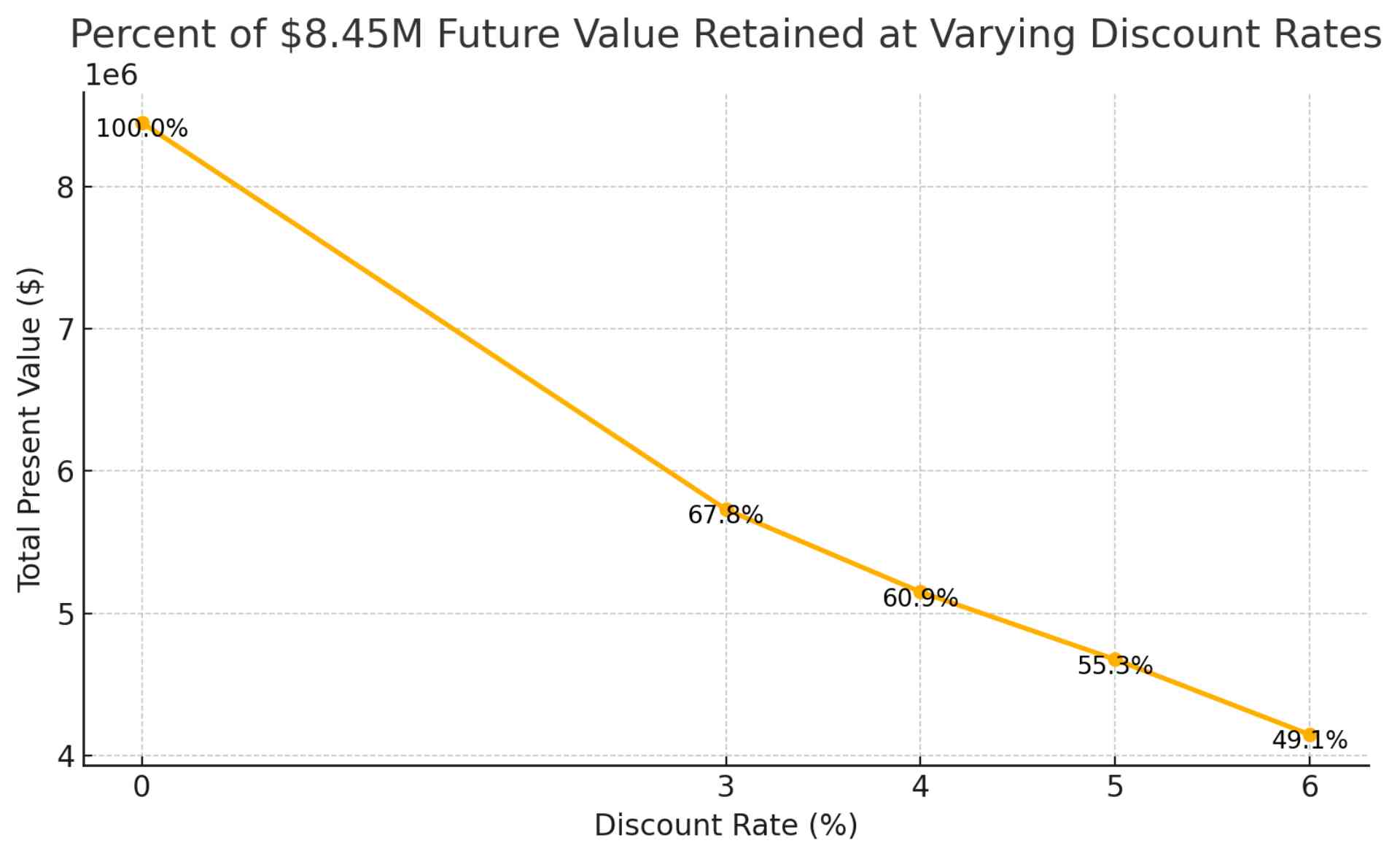

| Taylor v. FreightLine Logistics | ||||

| Damage Type | Future Amount | PV at 3% | PV at 6% | Difference |

|---|---|---|---|---|

| Lost Earnings (20 yrs at $80k/yr) | $1,600,000 | $1,189,177 | $917,594 | -$271,583 |

| Pension Benefits (15 yrs at $40k/yr) | $600,000 | $348,269 | $217,629 | -$130,640 |

| Earning Potential (non-employed youth) | $2,400,000 | $1,408,842 | $902,674 | -$506,168 |

| Medical & Life Care (25 yrs at $100k) | $2,500,000 | $1,741,020 | $1,278,534 | -$462,486 |

| Household Services (20 yrs at $30k/yr) | $600,000 | $446,786 | $344,098 | -$102,688 |

| Structured Settlement (15 yrs at $50k) | $750,000 | $596,203 | $485,576 | -$110,627 |

| Total Impact | $8,450,000 | $5,730,297 | $4,146,105 | – $1,584,192 |

Taylor, a 35-year-old construction worker, suffered permanent injuries in a collision with a FreightLine Logistics truck. The accident left Taylor unable to work, in need of lifelong care, and dependent on others for household tasks. The damages include lost earnings, diminished pension benefits, long-term medical expenses, and loss of household services.

Lost Wages and Earning Capacity

One of the most common categories affected by rising interest rates is lost wages and future earning capacity. Calculating these damages involves projecting the injured individual’s expected earnings and discounting them back to their present value. Rising interest rates directly impact the calculation, often reducing the present value of long-term wage losses.

Example:

Taylor’s injuries ended a promising career in construction, eliminating $1,600,000 in future earnings over 20 years. At a 3% discount rate, the present value is $1,189,177. At 6%, it drops to $917,594, a loss of over $270,000 in recoverable damages, showing how long-term wage loss claims shrink with rising interest rates, affecting both settlement value and trial risk.

Pension and Retirement Benefits

Interest rates significantly impact the valuation of lost pension and retirement benefits, especially in wrongful termination, wrongful death, or personal injury cases. These benefits often represent a significant component of economic damages, particularly for older workers nearing retirement or public-sector employees with defined benefit pensions. Higher interest rates typically decrease the present value of future pension benefits, given that retirement plans rely heavily on long-term financial projections.

Example:

Taylor also lost access to union pension benefits of $40,000 annually for 15 years beginning at age 65. At a 3% discount rate, that’s worth $348,269 today. At 6%, it falls to $217,629, reducing the valuation by over $130,000.

Loss of Earning Potential (Non-Employed Plaintiffs)

When calculating economic damages for plaintiffs who were not yet employed or who re-enter the workforce, rising interest rates can substantially affect the valuation of their lost earning potential. These cases often involve long time horizons, amplifying the impact of appropriate interest rate fluctuations. Since younger plaintiffs typically have decades of potential earnings ahead, even modest increases in discount rates can significantly reduce their damage awards.

Example:

In similar cases involving students or younger adults, projected earning losses are even more affected. A 20-year-old with $60,000 annually in expected earnings over 40 years would lose $506,000 in present value when discounting 6% instead of 3%.

Medical and Life Care Costs

Economic damages frequently include long-term medical and life care costs, especially in catastrophic injury cases. Rising interest rates significantly affect the calculation of these damages by reducing the present value of future medical expenses and care costs, even when inflation in healthcare costs is considered. When projecting life care plans, economists factor in healthcare inflation and discount rates. An increase in interest rates can decrease the lump sum needed today to fund future medical costs.

Example:

Taylor will need $100,000 annually in medical and assisted care over the next 25 years, totaling $2,500,000. At 3%, that’s worth $1,741,020 today. At 6%, the present value drops to $1,278,534, a difference of more than $460,000.

Loss of Household Services

In wrongful death or severe injury cases, damages frequently include the economic value of lost household services, such as childcare, cleaning, home maintenance, or caregiving. These services have real economic value and are calculated based on market rates for equivalent professional services. Rising interest rates directly affect these calculations by decreasing the present value of future household services lost. Higher discount rates reduce the lump-sum amount needed today to replace these services, particularly when they extend over many years.

Example:

Taylor’s injuries also prevent him from providing essential household services, valued at $30,000 annually over 20 years. At a 3% discount rate, the present value is $446,786. At 6%, it drops to $344,098, reducing compensation by over $100,000.

Structured Settlements and Annuities

Structured settlements and annuities are commonly used in personal injury cases to provide regular, long-term payments rather than a single lump sum and rely heavily on interest rates, which influence the cost and value of the annuity that funds future payments. Rising interest rates generally reduce the cost of structured settlements for defendants, making them more attractive for resolving claims. Conversely, plaintiffs considering structured settlements must understand how changing rates affect the value of payments offered by insurance companies or settlement providers.

Example:

If Taylor’s claim is resolved through a structured settlement paying $50,000 annually for 15 years, the cost to fund that annuity today would be $596,203 at 3%. At 6%, it drops to $485,576, saving the defense over $110,000.

Impact on Business and Property-Related Damages

In business and commercial litigation, future economic damages are discounted to present value using interest rates, meaning rate changes can significantly alter the valuation of lost profits, property damage, and other financial losses.

To illustrate how rising interest rates influence business-related economic damage calculations, we’ll examine a single, detailed hypothetical case:

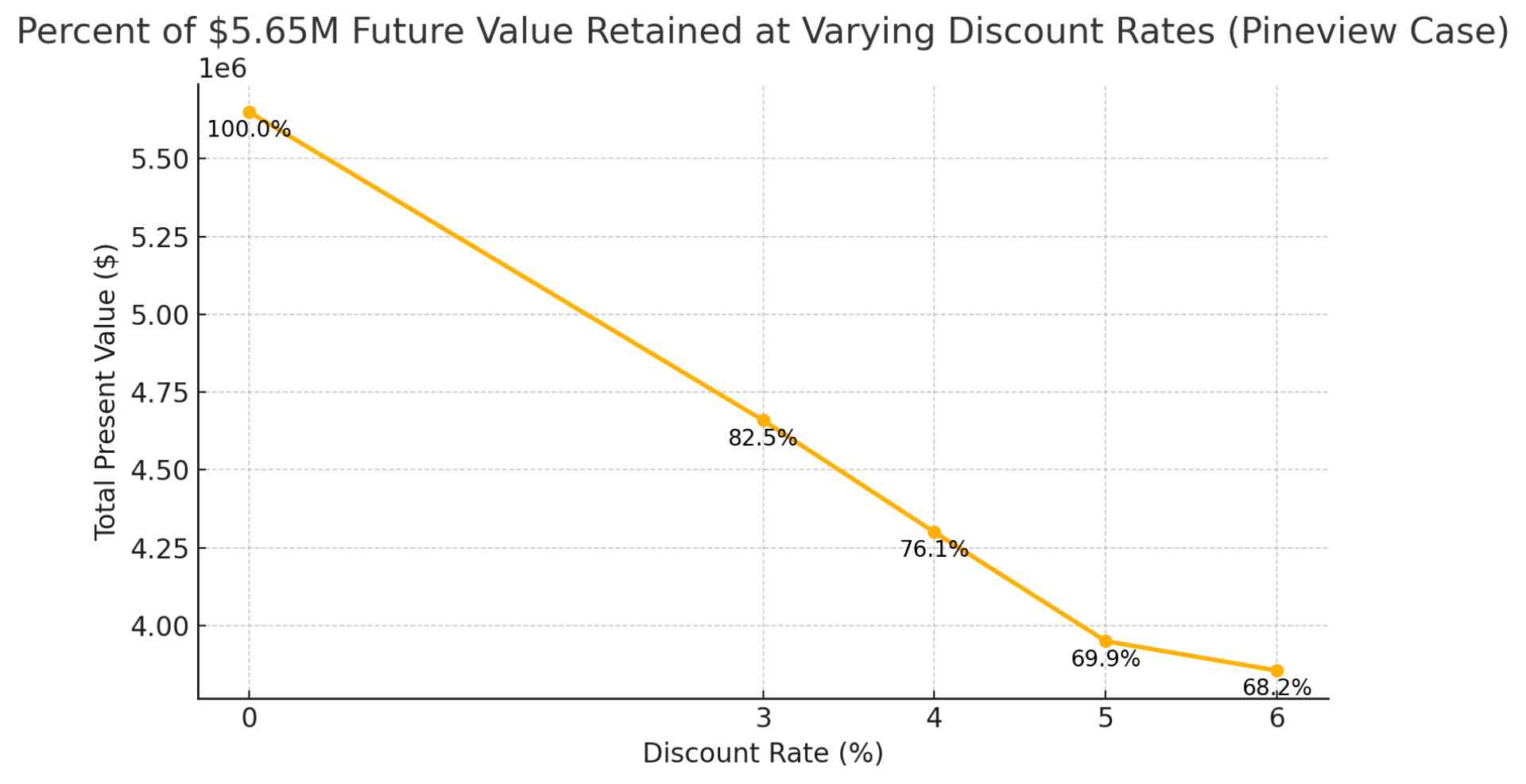

| Pineview Manufacturing v. Coastal Transport | ||||

| Damage Type | Future Amount | PV at 3% | PV at 6% | Difference |

|---|---|---|---|---|

| Lost Profits and Business Income | $1,200,000 | $1,182,330 | $1,104,622 | -$76,708 |

| Loss of Goodwill/Business Value | $1,500,000 | $1,193,778 | $971,225 | -$222,553 |

| Diminished Property Value | $1,000,000 | $743,874 | $573,496 | -$170,378 |

| Investment Losses/Opportunities | $1,200,000 | $858,485 | $587,123 | -$271,362 |

| Environmental Remediation | $400,000 | $372,068 | $346,535 | -$25,533 |

| Increased Financing Costs | $150,000 | $136,238 | $122,993 | -$13,245 |

| Contractual Penalties | $200,000 | $172,626 | $149,453 | -$23,173 |

| Total Impact | $5,650,000 | $4,659,399 | $3,855,447 | -$803,952 |

Pineview Manufacturing — a mid-sized equipment manufacturer — experienced significant economic losses due to a trucking accident and a chemical spill caused by Coastal Transport. The chemical spill forced Pineview to shut down operations temporarily, contaminated company property, disrupted production schedules, damaged customer relationships, and delayed planned business expansions.

Lost Profits and Business Income

One of the primary damage claims in business litigation is compensation for lost profits and business income resulting from disruption. Forensic economists discount these amounts to present value when projecting future lost profits. Rising interest rates, which result in higher discount rates, significantly decrease the present value calculation, directly affecting the size of awarded damages.

Example:

Pineview lost $1,200,000 in profits during a six-month shutdown and expects an additional $1,500,000 in future profit loss due to reputational harm. At a 3% discount rate, these losses are valued at $1,182,330 and $1,280,533, respectively. At 6%, the long-term portion drops to $1,104,622, reducing recoverable damages by nearly $176,000.

Loss of Goodwill or Reduced Business Value

Goodwill represents the intangible value of a business’s brand, reputation, and customer loyalty, critical factors often severely impacted by disruptive events. Forensic economists estimate the impact on future earnings when calculating damages related to lost goodwill or reduced business value and then discount these amounts back to present value. Rising interest rates tend to lower the valuation of goodwill damages, primarily when the impairment affects long-term customer relationships or market position.

Example:

After the spill, Pineview projects a $1,500,000 loss in future profits tied to damaged customer relationships. At a 3% discount rate, the present value is $1,193,778. At 6%, it drops to $971,225, reducing recoverable damages by over $220,000.

Diminished Property Value

Diminished property value damages occur when an event significantly reduces the market value or income-generating capacity of a business-owned asset, such as commercial real estate or machinery. Valuation often involves projecting the property’s reduced future earnings capacity or expected resale value and discounting these amounts to the present. Higher interest rates mean higher discount rates, substantially decreasing the calculated present value of future diminished property earnings or losses.

Example:

Contamination from the spill is expected to reduce Pineview’s ability to generate income from the property by $1,000,000 over 20 years. At a 3% discount rate, the present value is $743,874. At 6%, it falls to $573,496, lowering potential damages by about $170,000.

Investment Losses or Foregone Opportunities

Investment losses or foregone opportunities represent financial harm due to delayed or canceled projects resulting from business disruptions. When calculating these damages, economists project future profits or cost savings expected from planned investments and discount them to present value. Rising interest rates increase discount rates, reducing the present value of anticipated returns from these foregone business opportunities.

Example:

Pineview’s canceled expansion was expected to generate $1,200,000 in profits over 10 years, starting five years out. At a 3% discount rate, the present value is $858,485. At 6%, it drops to $587,123, reducing recoverable damages by more than $271,000.

Additional Damages to Consider

Beyond the primary damage categories, rising interest rates affect several other types of economic damages, which attorneys should keep in mind. These may include increased financing costs, contractual penalties, environmental remediation expenses, loss of intellectual property value, and supply chain disruption costs. Each involves future cash flows that, when discounted at higher rates, can substantially impact the total damage calculation.

Example:

Following Coastal Transport’s chemical spill, Pineview Manufacturing faced additional costs and losses.

- Environmental remediation costs: Pineview expects to incur $400,000 in cleanup expenses spread evenly over the next four years.

- Increased financing costs: Due to disrupted cash flow, Pineview required additional financing, resulting in $25,000 annually in increased interest payments for the next six years (totaling $150,000).

- Contractual penalties: Pineview owed a total of $200,000 in penalties payable five years from now due to delayed fulfillment of existing contracts.

As shown, rising interest rates reduced the combined present value of these additional damages by nearly $62,000. Attorneys representing plaintiffs and defendants must factor these less obvious damages into their strategic analyses, understanding how interest rates affect the final settlement or judgment value.

Interest Rates and Inflation: Not Always Aligned

A common misconception in economic damages litigation is that rising interest rates automatically imply rising inflation, which justifies applying higher discount rates. In reality, interest rates and inflation do not move in perfect lockstep.

A defensible economic damages model must distinguish between nominal and real discount rates and consider how each is derived.

- Nominal rates reflect the actual interest rate observed in the market — what you see in Treasury yields or bond rates.

- Real rates adjust for inflation and reflect the actual time value of money. Damage calculations are typically performed in real terms unless inflation is explicitly included in the projections.

Using a nominal discount rate on real (inflation-adjusted) earnings, or vice versa, results in inconsistent and misleading values. In high-interest environments, it’s especially important to clarify whether the wage growth rate, medical costs, and other projections are in real or nominal dollars and then align the discount rate accordingly.

In practice, observed market interest rates may also reflect a liquidity premium, then added return investors demand for assets that are not easily converted into cash. When applying discount rates to damage models, especially in long-term structured settlements or illiquid future obligations, it’s essential to assess whether the rate accounts for this liquidity risk or whether an adjustment is needed.

Why High Interest Rates Don’t Automatically Mean High Inflation

While the Federal Reserve raises interest rates in part to curb inflation, the policy goal is to reduce inflation and avoid financial crisis. As a result, rising interest rates may coincide with falling inflation expectations, meaning the real discount rate could increase significantly even if nominal inflation remains stable or drops.

A higher real discount rate might be appropriate in damage modeling, but only if the underlying assumptions about inflation, cost growth, and investment returns are appropriately adjusted and internally consistent.

Implications for Defensible Expert Modeling

Courts and opposing counsel often scrutinize the discount rate used in a damages analysis. A well-supported expert report must clearly identify whether damages are projected in nominal or real dollars; whether the discount rate aligns with that choice; and how current and expected inflation trends influence the rate selection.

Increased volatility in interest rates makes these distinctions even more critical. A forensic economist who fails to account for the interplay between interest rates and inflation risks produces flawed results that may be discredited in court.

Why Accurate Damage Modeling Matters More Than Ever

Rising interest rates aren’t just a financial headline. They directly affect the outcome of litigation. From long-term lost profits to property and investment damages, the discount rate applied to future losses can swing the value of a case by hundreds of thousands or even millions of dollars.

At The Knowles Group, we provide attorneys with expert economic analysis that holds up under scrutiny. If you’re working on a case where lost future earnings are a key issue, contact us for a free case consultation to ensure your damage model reflects the most current and defensible assumptions backed by real-world data and courtroom experience.